Commodities 2023, 2(3), 280-311; https://doi.org/10.3390/commodities2030017 - 31 Aug 2023

Abstract

►

Show Figures

This paper applies a two-tier model based on fuel hedging (model 1) and the testing of the impact of commodity risk on airline capacity forecasting, which is based on a system dynamics framework (model 2). Model 1 provides a comprehensive examination of the

[...] Read more.

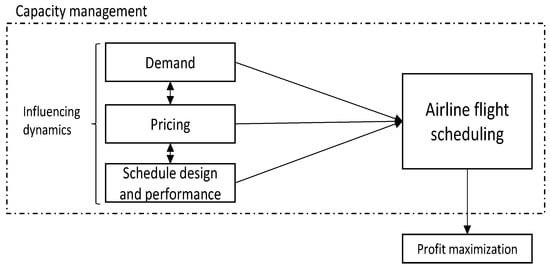

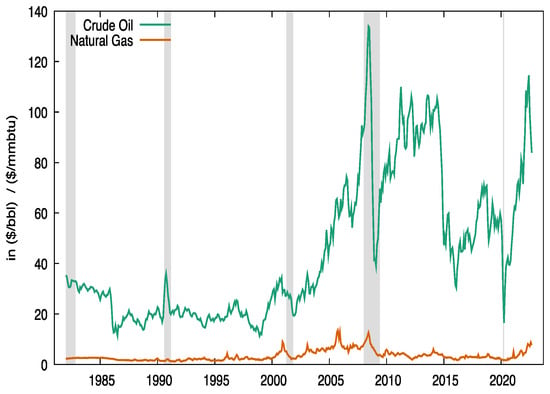

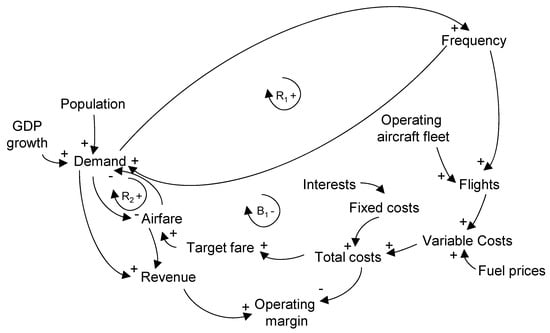

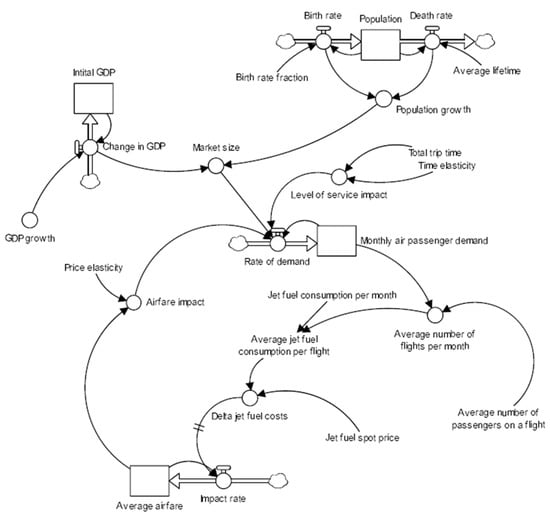

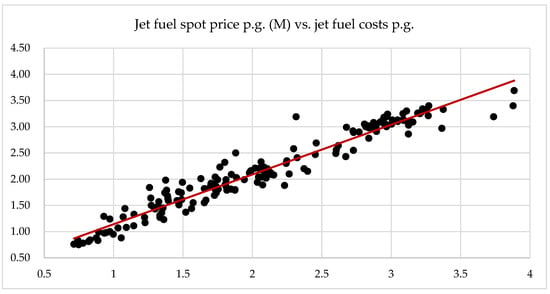

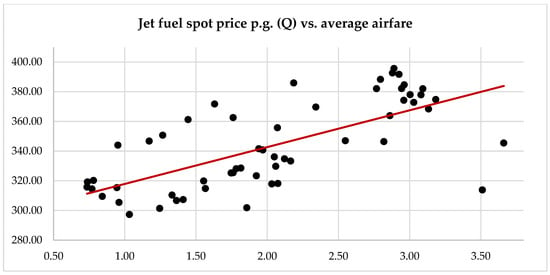

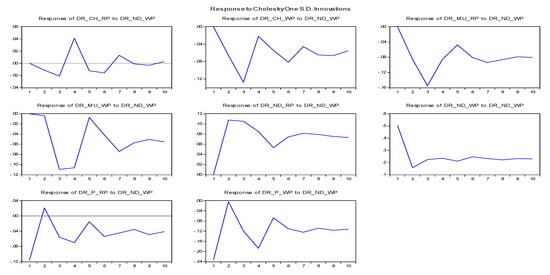

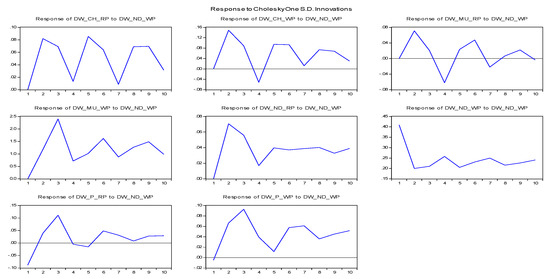

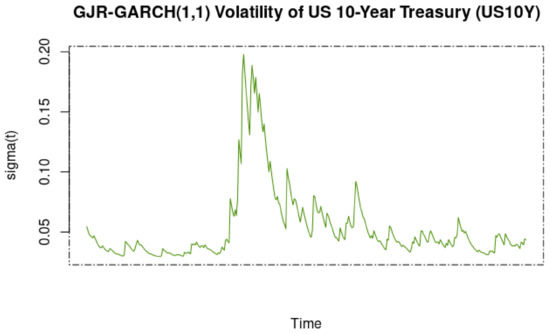

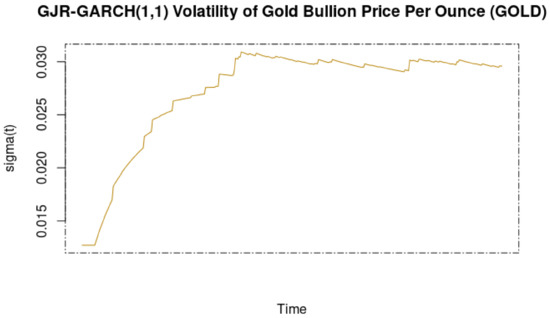

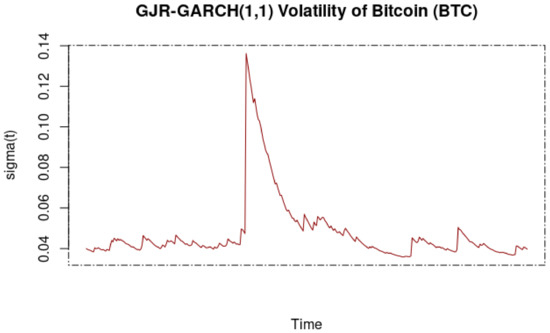

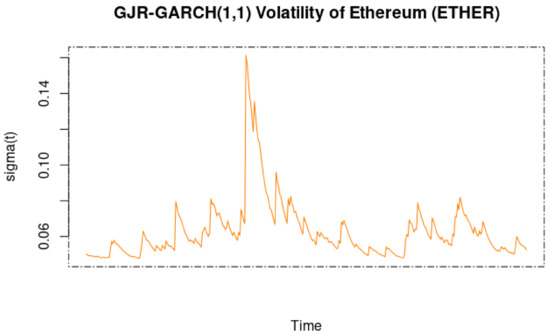

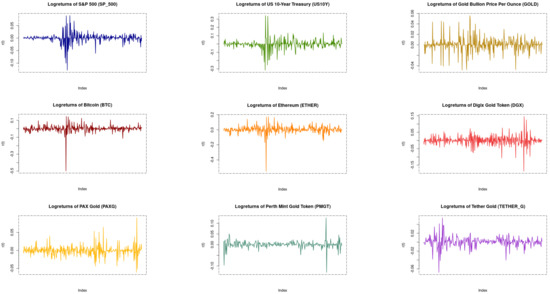

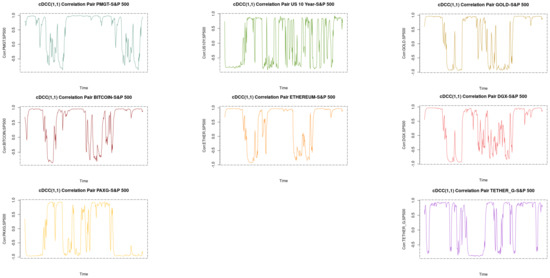

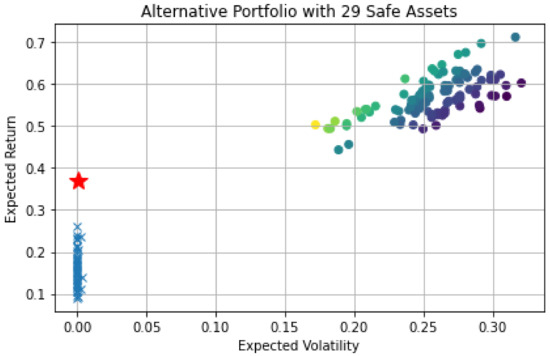

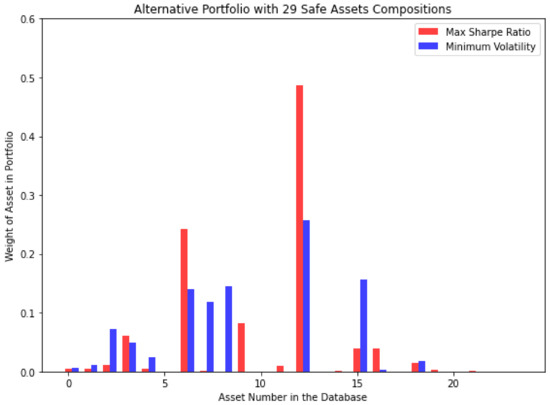

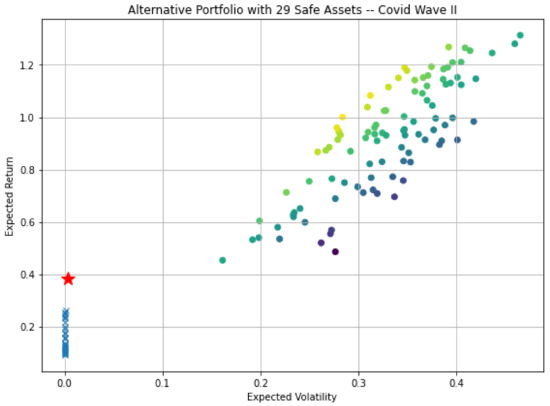

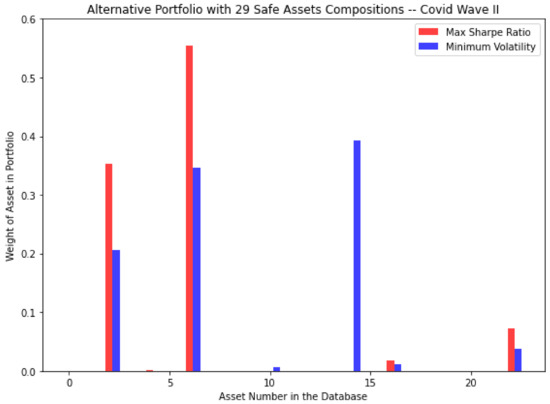

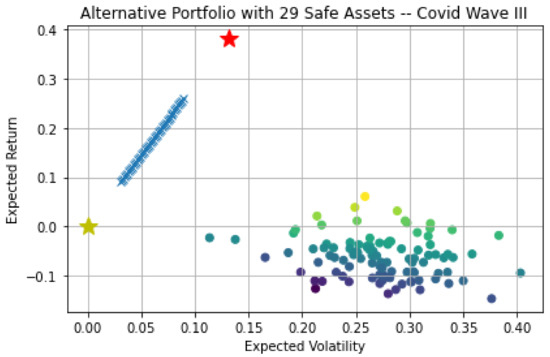

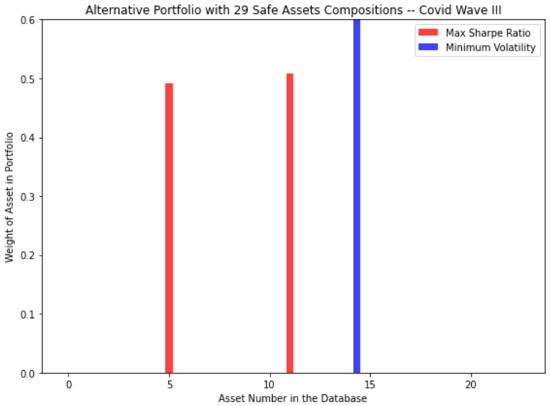

This paper applies a two-tier model based on fuel hedging (model 1) and the testing of the impact of commodity risk on airline capacity forecasting, which is based on a system dynamics framework (model 2). Model 1 provides a comprehensive examination of the worldwide airline industry, including an analysis of the statistical impact of oil price fluctuations on the sector and the corresponding hedging strategies employed by airlines. This study examines a sample of North American and European airlines over a 10-year timeframe to assess the degree to which these airlines have engaged in kerosene hedging for future periods and the potential impact of such hedging on their corporate value and performance. In model 2, the author integrates a capacity-forecasting model within the system dynamics framework, drawing upon the theory of capacity forecasting. The study examines the impact of commodity risk by analysing the influence of fluctuations in the jet fuel spot price on the average airfare and its subsequent effects on other interdependent capacity variables. The hypotheses presented in this study were formulated based on a comprehensive review of the relevant literature and a causal feedback loop diagram. The diagram effectively depicts the dynamic interrelationships between capacity forecasting and risk variables. Furthermore, the diagram capturing causal feedback loops was transformed into a stock-flow diagram. This diagram was then utilised to evaluate the hypotheses that were derived using a dataset that pertains to the domestic airline market in the United States. The verification of the qualitative and quantitative models demonstrates the proven impact of commodity risk on capacity forecasting.

Full article

Figure 1

.jpg)

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}