by

, , , and

J. Risk Financial Manag. 2023, 16(9), 390; https://doi.org/10.3390/jrfm16090390 - 31 Aug 2023

Abstract

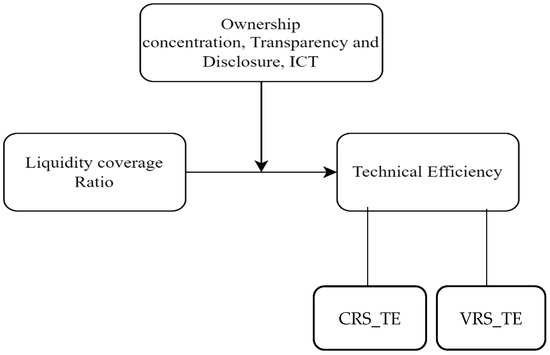

The current study investigates the impact of the liquidity coverage ratio (LCR) on the efficiency of Indian banks for the period 2010 to 2019. The study examines the effect of internal bank elements like ownership structure, transparency and disclosure, and technological advancement on

[...] Read more.

The current study investigates the impact of the liquidity coverage ratio (LCR) on the efficiency of Indian banks for the period 2010 to 2019. The study examines the effect of internal bank elements like ownership structure, transparency and disclosure, and technological advancement on the relationship between the LCR and efficiency. Bank efficiency proxied as technical efficiency is evaluated by applying the data envelope analysis approach. Applying the panel data regression technique, the authors discover that the LCR has a positive impact on the technical efficiency at a constant return to scale of banks. The relationship between the LCR and the technical efficiency at a variable return to scale is non-linear. Initially, as liquidity increases, the efficiency of banks improves, after reaching its optimum level, efficiency starts to decline. Furthermore, liquidity tends to improve efficiency of banks with higher promoter stakes, whereas opposing results are evidenced for institutional investors and technological advancement.

Full article

(This article belongs to the Special Issue Corporate Finance: Financial Management of the Firm)

►

Show Figures

Figure 1

.gif)

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}